On Sept 7, US President Donald Trump announced that he was looking at the possibility of imposing an additional tariff on $267 billion of Chinese exports to the United States. This move will be the third in a series of tariff hikes targeting Chinese imports to the US: The first on $50 billion of imports was implemented in two phases over July and August, and the second stage of $200 billion had just completed the public hearing process with final product list decision coming anytime. Trump already announced that he would approve the tariff “very soon” after he gets the final list. The recent announcement of $267 billion will be the third stage and essentially cover all imports from China.

Based on the classification of the US imports from China from Deutsche Bank, the US tariff decision has two characteristics: The first is the tariff structure favors consumer goods over non-consumer goods, and the second is the tariff design will cause increasing marginal pain to the US economy.

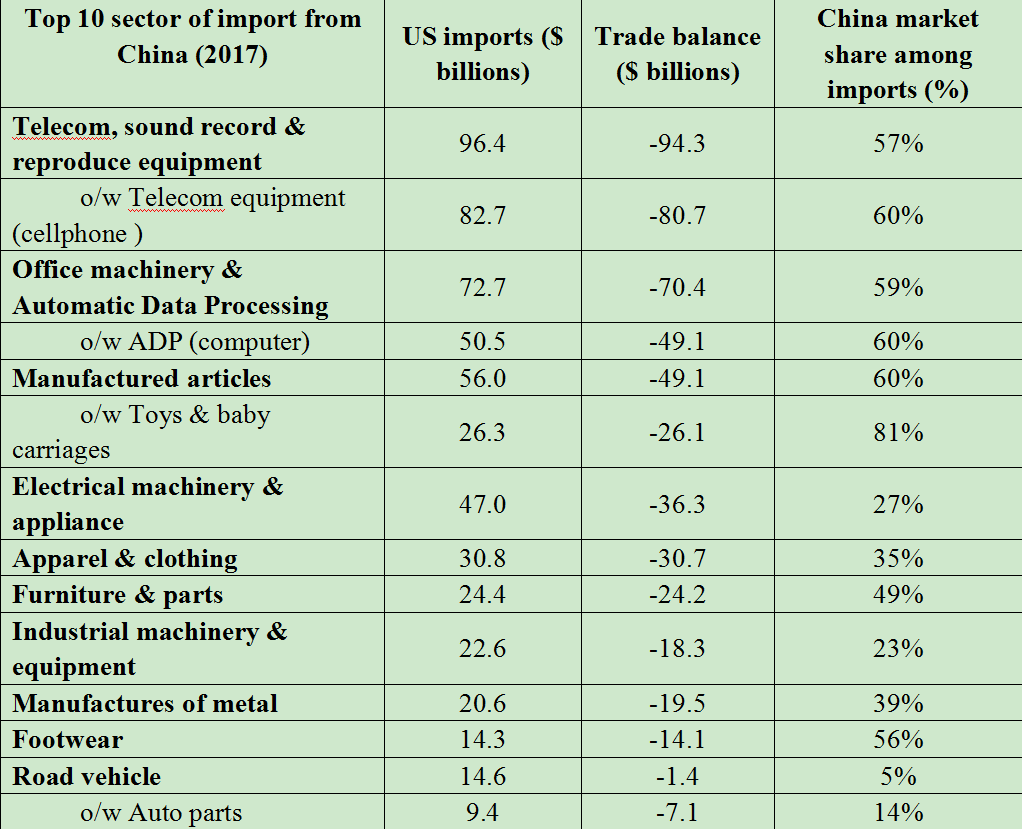

Figure 1: Top 10 imports of the US from China and its market share among imports in 2017

Figure 1 shown the top 10 import of the US from China and two outstanding features comes out: The first is the high China import market share in the particular import category; four categories have market share more than 50 percent, five groups have a market share between 20 percent and 50 percent, with only the 10th group, under road vehicles, is insignificant at 5 percent. High import share in the overall importation means the country enjoys comparative production advantage in the international trade arena on these products. Trying to replace these products by substituting with local production or alternative import sources is not realistic in the short run. The new supply chain to build these products takes time to develop, and they are more expensive if produced elsewhere. The top two import categories are high-tech products that are sensitive to quality issue in which supply chain buildup is particularly time-consuming. The Chinese move in recent years from the Original Equipment Manufacturing (OEM) to Original Design Manufacturing (ODM) and onshoring of upstream parts means the deep integration of these products to the production network in China. The tariff wall on these products in the absence of alternate supply sources implies merely the tariff passing through and higher price to consumers.

The second feature is that many of these products are intermediate or non-consumer goods. They are inputs to other industries and slapping a tariff on them will hurt the downstream industries that rely on them as input.

Figure 2: US tariff hike stages and percentage of non-consumer goods

The first tariff conundrum of favoring consumer goods over intermediate goods as shown in figure 2 is designed to minimize the inflation impact on the economy. However, letting the intermediate products carry the burden of tariffs deprives the economy of the benefit of value-added opportunity over the imported goods and the multiplier benefit that intermediate goods generate for the economy is lost. Conventional wisdom usually favors non-consumer goods over consumer goods in a tariff war, and the current setup defies economic logic. US icon Harvey-Davidson moving its export base from the US to Thailand after the steel tariff imposition is a case in hand.

The second characteristics of the US tariff decision are that the tariff design will cause increasing marginal pain to the US economy. Figure 3 on the three stages of tariff hikes clearly shows that each succeeding tariff stage will put goods with higher Chinese import concentration groups into the tariff hike. Higher Chinese import market share means increasingly poor substitutability for the Chinese imported products. The marginal cost to the US economy will increase with each tariff hike, particularly on the inflation side. The recent hearing on the second phase of tariff hikes has witnessed an increasing number of high-tech companies from Intel to Apple voicing its opposition. If one still wants to escalate the trade war in the face of the higher marginal cost to the economy is undoubtedly defying economic logic.

Figure 3: US tariff hike stages and percentage of Chinese import

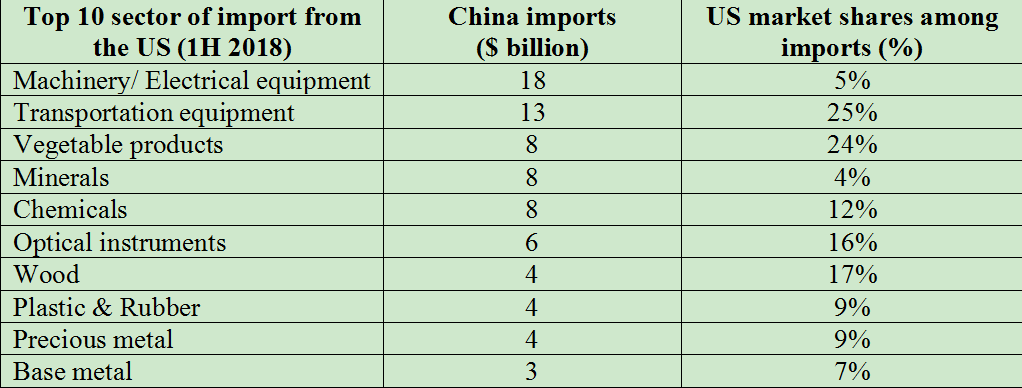

The Chinese situation in the current trade war is better than the US only so far as the primary effect is a concern. Figure 4 shows that the country’s import dependency ratio on the top 10 imported goods from the US is relatively low, the country can quickly source the products elsewhere. On the well-known disruption case of ZTE, the shock to the company is more on parts disruption and the time-consuming process of validating alternative parts in the sophisticated products. Hence any supply disruption based on tariff hike on US goods is minimal. On the vegetable products which is essentially soybean, China already implemented the tariff hike, and any marginal cost to the Chinese economy henceforth is minimal.

Figure 4: Top 10 imports of China from the US and their market shares among import in first half of 2018

The immediate economic impact on China is the loss of the trade surplus with the US and over the long run, a global supply chain migration out of the country. Of course, whether there will be any secondary effect remains an unknown, but the Chinese government gets time to look over these effects and use the policy tools on its hand to contain them.

The announcement that US Treasury Secretary Mnuchin is inviting the Chinese side to resume the negotiation and the favorable response from China is a good sign that both sides are willing to talk and hopefully, set aside differences over non-economic issues to reach a “win-win” resolution over the current “no winner” situation.

Henry Chan is a visiting researcher at East Asia Institute, National University of Singapore. The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.

Henry Chan

On Sept 7, US President Donald Trump announced that he was looking at the possibility of imposing an additional tariff on $267 billion of Chinese exports to the United States. This move will be the third in a series of tariff hikes targeting Chinese imports to the US: The first on $50 billion of imports was implemented in two phases over July and August, and the second stage of $200 billion had just completed the public hearing process with final product list decision coming anytime. Trump already announced that he would approve the tariff “very soon” after he gets the final list. The recent announcement of $267 billion will be the third stage and essentially cover all imports from China.

Based on the classification of the US imports from China from Deutsche Bank, the US tariff decision has two characteristics: The first is the tariff structure favors consumer goods over non-consumer goods, and the second is the tariff design will cause increasing marginal pain to the US economy.

Figure 1: Top 10 imports of the US from China and its market share among imports in 2017

Figure 1 shown the top 10 import of the US from China and two outstanding features comes out: The first is the high China import market share in the particular import category; four categories have market share more than 50 percent, five groups have a market share between 20 percent and 50 percent, with only the 10th group, under road vehicles, is insignificant at 5 percent. High import share in the overall importation means the country enjoys comparative production advantage in the international trade arena on these products. Trying to replace these products by substituting with local production or alternative import sources is not realistic in the short run. The new supply chain to build these products takes time to develop, and they are more expensive if produced elsewhere. The top two import categories are high-tech products that are sensitive to quality issue in which supply chain buildup is particularly time-consuming. The Chinese move in recent years from the Original Equipment Manufacturing (OEM) to Original Design Manufacturing (ODM) and onshoring of upstream parts means the deep integration of these products to the production network in China. The tariff wall on these products in the absence of alternate supply sources implies merely the tariff passing through and higher price to consumers.

The second feature is that many of these products are intermediate or non-consumer goods. They are inputs to other industries and slapping a tariff on them will hurt the downstream industries that rely on them as input.

Figure 2: US tariff hike stages and percentage of non-consumer goods

The first tariff conundrum of favoring consumer goods over intermediate goods as shown in figure 2 is designed to minimize the inflation impact on the economy. However, letting the intermediate products carry the burden of tariffs deprives the economy of the benefit of value-added opportunity over the imported goods and the multiplier benefit that intermediate goods generate for the economy is lost. Conventional wisdom usually favors non-consumer goods over consumer goods in a tariff war, and the current setup defies economic logic. US icon Harvey-Davidson moving its export base from the US to Thailand after the steel tariff imposition is a case in hand.

The second characteristics of the US tariff decision are that the tariff design will cause increasing marginal pain to the US economy. Figure 3 on the three stages of tariff hikes clearly shows that each succeeding tariff stage will put goods with higher Chinese import concentration groups into the tariff hike. Higher Chinese import market share means increasingly poor substitutability for the Chinese imported products. The marginal cost to the US economy will increase with each tariff hike, particularly on the inflation side. The recent hearing on the second phase of tariff hikes has witnessed an increasing number of high-tech companies from Intel to Apple voicing its opposition. If one still wants to escalate the trade war in the face of the higher marginal cost to the economy is undoubtedly defying economic logic.

Figure 3: US tariff hike stages and percentage of Chinese import

The Chinese situation in the current trade war is better than the US only so far as the primary effect is a concern. Figure 4 shows that the country’s import dependency ratio on the top 10 imported goods from the US is relatively low, the country can quickly source the products elsewhere. On the well-known disruption case of ZTE, the shock to the company is more on parts disruption and the time-consuming process of validating alternative parts in the sophisticated products. Hence any supply disruption based on tariff hike on US goods is minimal. On the vegetable products which is essentially soybean, China already implemented the tariff hike, and any marginal cost to the Chinese economy henceforth is minimal.

Figure 4: Top 10 imports of China from the US and their market shares among import in first half of 2018

The immediate economic impact on China is the loss of the trade surplus with the US and over the long run, a global supply chain migration out of the country. Of course, whether there will be any secondary effect remains an unknown, but the Chinese government gets time to look over these effects and use the policy tools on its hand to contain them.

The announcement that US Treasury Secretary Mnuchin is inviting the Chinese side to resume the negotiation and the favorable response from China is a good sign that both sides are willing to talk and hopefully, set aside differences over non-economic issues to reach a “win-win” resolution over the current “no winner” situation.

Henry Chan is a visiting researcher at East Asia Institute, National University of Singapore. The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.