By Henry Chan |

chinawatch.cn |

Updated: 2018-10-09 17:18

Henry Chan

In 1965, then French Finance Minister Valery Giscard d'Estaing described the pivotal role of the US dollar in the global financial system set up by the 1944 Bretton Woods agreement as an “exorbitant privilege”.

Under the 1944 agreement the US dollar earned the role of global reserve currency based on the US government guaranteed convertibility of the money to gold. The reserve currency status allows the US to finance its trade and budget deficit easily and protects the country against balance-of-payment crises because it imports and services borrowing in its currency. The pivotal position of the US dollar allows it to become the global trade pricing currency, dominate cross-country borrowing and the country’s monetary policies, such as quantitative easing, influence global interest rate and affects the economies of other countries.

Although President Richard Nixon ended the official link between the US dollar and gold in 1971, the “Nixon shock” unintentionally removed any restraint on the monetary policy of the US and allowed the country to control the supply of the currency. The advent of the Eurodollar and Asian dollar in the 1960s to accommodate the monetary expansion of the US enhanced the role of the US dollar in third-party transactions and increases the presence of the currency worldwide.

While the traditional role played by a reserve currency is as a medium of transaction, the US dollar became increasingly important in the store of value and unit of account function from the 1970s following the recycling of petrodollars, expansion of the global monetary base and increasing cross-border global capital flow.

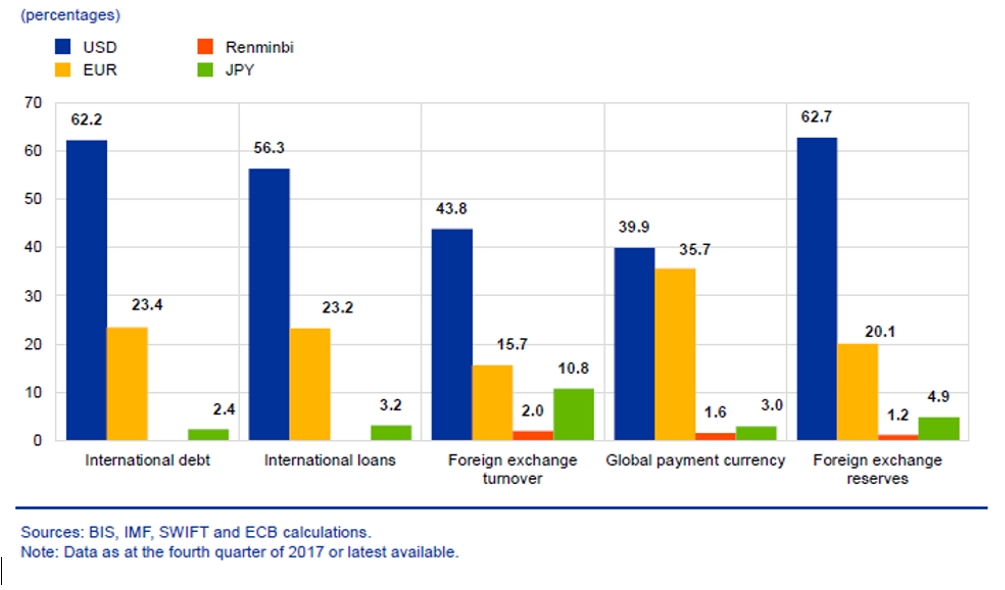

Figure 1: The global financial system based on currency use. Source: ECB

Figure 1 shows the dominance of the US dollar in the global financial system. The US accounts for 23 percent of global nominal GDP, but the dollar accounts for a much higher share of global financial flow.

The increasing role the US dollar plays presents a problem to the world. The dual mandate on the gatekeeper of the US monetary policy, the US Federal Reserve, is to maximize employment and stabilize prices. The mandate excludes any reference to global financial stability and growth. The domestic orientation of US monetary policy has created severe adjustment issues for other countries whose currencies are considered dollar-linked, particularly developing countries.

Whenever the Fed reduces interest rates in response to the domestic economic slowdown, liquidity flows to developing countries to take advantage of rate differentials. The flow often takes the form of US dollar denominated debt. With the ultimate reversal of the interest rate cycle by the Fed when the country’s economy recovers, the same developing countries experience a capital flight to the safety of the US dollar. The reason is that when the dollar strengthens, the volume of debt that emerging markets have sold in dollars, rather than their local currency, becomes more expensive and harder to pay back, which makes investors fearful. The subsequent drain of liquidity creates depreciation pressure and capital flight with a depressing effect on their economy.

The longer the US rate cycle and sharper peak to trough, the monetary policy spillover effect of the US dollar on developing countries is more pronounced. The boom and bust of some developing countries’ economy mirroring the US interest rate cycle is well documented in every rate cycle since the 1970s. The statement of the US treasury secretary John Connally in 1971, “The dollar is our currency, but it’s your problem” aptly described the conundrum of the US dollar in the international financial system.

The present high use of the dollar in figure 1 reflects the absence of serious competitors to the currency at the moment. The ascendancy of the Japanese yen in the 1980s and the euro in the 1990s has not dented the importance of the US dollar in the global financial system. These two currencies failed to replace the pivotal role of the US dollar following the lost decades of the Japanese economy and the Greek crisis that exposed the structural weakness of the euro. That of the world’s second-largest economy, China’s renminbi, suffers from a closed capital account and the country’s financial sector reform is, at best, just half done and lacks the breadth and depth for a reserve currency.

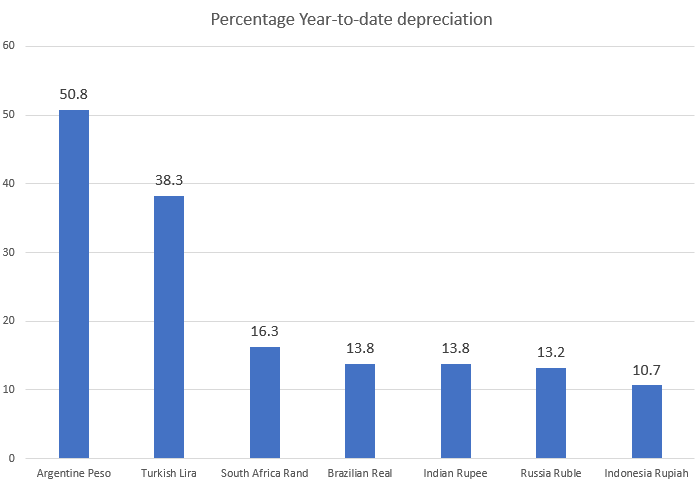

Since 2016 US rates have moved from 0.25 percent to 2 percent, with six rises in total. That has caused a run on emerging market currencies this year. There were seven countries whose exchange rate had depreciated more than 10 percent year-to-date until Oct 7 against the US dollar and they are all developing countries. Five of these countries are the original “fragile five” in 2015 with Argentina and Russia joining the rank to make it the “fragile seven”.

Figure 2: year-to-date percentage exchange rate change against US dollar to Oct 7.

From exorbitant privilege to weaponizing finance

The term weaponization of finance was suggested by Eurasia Group's Ian Bremmer and Cliff Kupchan in its Top Risk 2015 report. The report said the US under President Barack Obama was finding a new way to advance its geopolitical interest using its privileged position in the global financial system. The weaponization of finance refers to the foreign policy strategy of using financial incentives (access to capital markets) and penalties (varied types of sanctions) as tools of coercive diplomacy. Rather than relying on traditional elements of the US security advantage – including US-led alliances such as NATO and multilateral institutions such as the World Bank and the International Monetary Fund – Washington is weaponizing finance by limiting access to the US marketplace and US banks as an instrument of its foreign and security policy.

The US has a long history of using sanctions against adversaries. Earlier legislation such as the International Emergency Economic Powers Act, 1977, the Trading With the Enemy Act 1917, 1939, 1942 and the Patriot Act, 2001, allows Washington to weaponize payment flows. The US government usually applies these laws carefully with little controversy.

The scope of the US sanction often includes persons, entities, organizations, a regime or an entire country. Primary sanctions restrict rate flow typically, and secondary curbs limit foreign corporations, financial institutions and individuals from doing business with sanctioned entities. Any dollar payment flowing through a US bank or the American payments system provides the necessary nexus for the US to prosecute the offender or act against its American assets.

The secondary scope gives the nation extraterritorial reach over non-Americans trading with or financing a sanctioned party. The mere threat of prosecution can destabilize finances, trade and currency markets, effectively disrupting the activities of non-Americans even the entity was not in violation of laws where it was domiciled or operated, and the proscribed acts took place outside the US.

This leverage over third-country corporates has frightened many large multinationals and forced them to adopt business policies of the US.

The US sanction punishment is real. BNP Paribas paid $9 billion in fines and was suspended from dollar clearing for one year for violating sanctions against Iran, Cuba and Sudan. HSBC, Standard Chartered and many other banks have paid hefty fines for similar breaches.

President Trump, compared with his predecessors, is very active in using the weaponization of the dollar program to preserve the country’s global economic and geopolitical position. Apart from using existing laws, the just signed Countering America’s Adversaries through Sanctions Act extended that armoury.The expansion of sanctions from primary sanctions to secondary sanctions in recent years has created a long-term disincentive on the use of US dollars for international transactions.

European Union moves on Special Purpose Vehicle

The US announced on May 8 this year that the country is withdrawing from the Iranian nuclear deal and reimposing sanctions on Iran. The first phase of the ban that came into effect in August included restrictions on the Iranian purchase of US dollars, trade in gold and other precious metals and the sale to Iran of car parts, commercial aircraft and related parts and services. The second set of sanctions will come into effect on November 4 and restricts sales of oil and petrochemical products from Iran.

US sanctions on Iran also bar foreign firms that do business there from accessing the entire US banking and financial system. They cannot use US dollars in their transactions. The move is designed to paralyze the Iranian economy and force the country to renegotiate the nuclear deal.

The EU, expressing its disapproval of the US action, announced on Sept 25 that it would set up the euro-based Special Purpose Vehicle payment system before Nov 4 to facilitate legitimate trade between European companies and Iran. The other signatories to the original P5+1+EU agreement (the five permanent members of the United Nations Security Council – Britain, China, France, Russia, the US, plus Germany) – with Iran, China and Russia supported the EU move. China and the EU are Iran’s two biggest trading partners, and they accounted for more than half of Iran’s foreign trade last year. Their move could mean that Iran is unlikely to be paralyzed by the US sanction and forced back to the negotiation table any time soon.

Long-term implications for US dollar

The unprecedented EU action on Iranian trade in the face of US sanctions presents a long-term challenge to the pre-eminent position of the US dollar in the global financial system. The euro is a close second to the US dollar in global payment, as figure 1 shows, and if the Special Purpose Vehicle sponsored by the EU succeeds in preserving Iran’s foreign trade, some other countries could follow. If the list of countries the US imposes sanctions on keeps rising under President Trump’s administration, then there could be a tendency to move away from the US dollar as a medium of exchange in the global financial system and hurt the currency in the long run.

The pre-eminent position of the US dollar on international debt issuance, international loans, foreign exchange turnover and foreign exchange reserves often reflects the role of that of a vehicle currency. In the international debt in US dollars raised by company X in country A used for its project in country B, the USD's role is that of a vehicle currency to facilitate the investment and does not reflect any economic activities associated with the US. The situation is akin to the petrodollar's role after the oil crises. The extension of US sanctions to too many countries could discourage its use as a means of stored value by those countries.

There is no imminent challenger to the role of US dollar in the world today; no other currency can provide the US dollar liquidity on global financial transactions at the moment. The exorbitant privilege enjoyed by the US dollar has been there for more than half a century since the 1965 complaint, and it persists. However, the combined effect of exorbitant privilege and weaponization of the dollar could hurt the role of the US dollar in the long run. Whether the current dollar weaponization will or will not overstretch the said privilege remains to be seen.

Henry Chan is visiting senior research fellow at Cambodia Institute for Development and Peace. The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.

Henry Chan

In 1965, then French Finance Minister Valery Giscard d'Estaing described the pivotal role of the US dollar in the global financial system set up by the 1944 Bretton Woods agreement as an “exorbitant privilege”.

Under the 1944 agreement the US dollar earned the role of global reserve currency based on the US government guaranteed convertibility of the money to gold. The reserve currency status allows the US to finance its trade and budget deficit easily and protects the country against balance-of-payment crises because it imports and services borrowing in its currency. The pivotal position of the US dollar allows it to become the global trade pricing currency, dominate cross-country borrowing and the country’s monetary policies, such as quantitative easing, influence global interest rate and affects the economies of other countries.

Although President Richard Nixon ended the official link between the US dollar and gold in 1971, the “Nixon shock” unintentionally removed any restraint on the monetary policy of the US and allowed the country to control the supply of the currency. The advent of the Eurodollar and Asian dollar in the 1960s to accommodate the monetary expansion of the US enhanced the role of the US dollar in third-party transactions and increases the presence of the currency worldwide.

While the traditional role played by a reserve currency is as a medium of transaction, the US dollar became increasingly important in the store of value and unit of account function from the 1970s following the recycling of petrodollars, expansion of the global monetary base and increasing cross-border global capital flow.

Figure 1: The global financial system based on currency use. Source: ECB

Figure 1 shows the dominance of the US dollar in the global financial system. The US accounts for 23 percent of global nominal GDP, but the dollar accounts for a much higher share of global financial flow.

The increasing role the US dollar plays presents a problem to the world. The dual mandate on the gatekeeper of the US monetary policy, the US Federal Reserve, is to maximize employment and stabilize prices. The mandate excludes any reference to global financial stability and growth. The domestic orientation of US monetary policy has created severe adjustment issues for other countries whose currencies are considered dollar-linked, particularly developing countries.

Whenever the Fed reduces interest rates in response to the domestic economic slowdown, liquidity flows to developing countries to take advantage of rate differentials. The flow often takes the form of US dollar denominated debt. With the ultimate reversal of the interest rate cycle by the Fed when the country’s economy recovers, the same developing countries experience a capital flight to the safety of the US dollar. The reason is that when the dollar strengthens, the volume of debt that emerging markets have sold in dollars, rather than their local currency, becomes more expensive and harder to pay back, which makes investors fearful. The subsequent drain of liquidity creates depreciation pressure and capital flight with a depressing effect on their economy.

The longer the US rate cycle and sharper peak to trough, the monetary policy spillover effect of the US dollar on developing countries is more pronounced. The boom and bust of some developing countries’ economy mirroring the US interest rate cycle is well documented in every rate cycle since the 1970s. The statement of the US treasury secretary John Connally in 1971, “The dollar is our currency, but it’s your problem” aptly described the conundrum of the US dollar in the international financial system.

The present high use of the dollar in figure 1 reflects the absence of serious competitors to the currency at the moment. The ascendancy of the Japanese yen in the 1980s and the euro in the 1990s has not dented the importance of the US dollar in the global financial system. These two currencies failed to replace the pivotal role of the US dollar following the lost decades of the Japanese economy and the Greek crisis that exposed the structural weakness of the euro. That of the world’s second-largest economy, China’s renminbi, suffers from a closed capital account and the country’s financial sector reform is, at best, just half done and lacks the breadth and depth for a reserve currency.

Since 2016 US rates have moved from 0.25 percent to 2 percent, with six rises in total. That has caused a run on emerging market currencies this year. There were seven countries whose exchange rate had depreciated more than 10 percent year-to-date until Oct 7 against the US dollar and they are all developing countries. Five of these countries are the original “fragile five” in 2015 with Argentina and Russia joining the rank to make it the “fragile seven”.

Figure 2: year-to-date percentage exchange rate change against US dollar to Oct 7.

From exorbitant privilege to weaponizing finance

The term weaponization of finance was suggested by Eurasia Group's Ian Bremmer and Cliff Kupchan in its Top Risk 2015 report. The report said the US under President Barack Obama was finding a new way to advance its geopolitical interest using its privileged position in the global financial system. The weaponization of finance refers to the foreign policy strategy of using financial incentives (access to capital markets) and penalties (varied types of sanctions) as tools of coercive diplomacy. Rather than relying on traditional elements of the US security advantage – including US-led alliances such as NATO and multilateral institutions such as the World Bank and the International Monetary Fund – Washington is weaponizing finance by limiting access to the US marketplace and US banks as an instrument of its foreign and security policy.

The US has a long history of using sanctions against adversaries. Earlier legislation such as the International Emergency Economic Powers Act, 1977, the Trading With the Enemy Act 1917, 1939, 1942 and the Patriot Act, 2001, allows Washington to weaponize payment flows. The US government usually applies these laws carefully with little controversy.

The scope of the US sanction often includes persons, entities, organizations, a regime or an entire country. Primary sanctions restrict rate flow typically, and secondary curbs limit foreign corporations, financial institutions and individuals from doing business with sanctioned entities. Any dollar payment flowing through a US bank or the American payments system provides the necessary nexus for the US to prosecute the offender or act against its American assets.

The secondary scope gives the nation extraterritorial reach over non-Americans trading with or financing a sanctioned party. The mere threat of prosecution can destabilize finances, trade and currency markets, effectively disrupting the activities of non-Americans even the entity was not in violation of laws where it was domiciled or operated, and the proscribed acts took place outside the US.

This leverage over third-country corporates has frightened many large multinationals and forced them to adopt business policies of the US.

The US sanction punishment is real. BNP Paribas paid $9 billion in fines and was suspended from dollar clearing for one year for violating sanctions against Iran, Cuba and Sudan. HSBC, Standard Chartered and many other banks have paid hefty fines for similar breaches.

President Trump, compared with his predecessors, is very active in using the weaponization of the dollar program to preserve the country’s global economic and geopolitical position. Apart from using existing laws, the just signed Countering America’s Adversaries through Sanctions Act extended that armoury.The expansion of sanctions from primary sanctions to secondary sanctions in recent years has created a long-term disincentive on the use of US dollars for international transactions.

European Union moves on Special Purpose Vehicle

The US announced on May 8 this year that the country is withdrawing from the Iranian nuclear deal and reimposing sanctions on Iran. The first phase of the ban that came into effect in August included restrictions on the Iranian purchase of US dollars, trade in gold and other precious metals and the sale to Iran of car parts, commercial aircraft and related parts and services. The second set of sanctions will come into effect on November 4 and restricts sales of oil and petrochemical products from Iran.

US sanctions on Iran also bar foreign firms that do business there from accessing the entire US banking and financial system. They cannot use US dollars in their transactions. The move is designed to paralyze the Iranian economy and force the country to renegotiate the nuclear deal.

The EU, expressing its disapproval of the US action, announced on Sept 25 that it would set up the euro-based Special Purpose Vehicle payment system before Nov 4 to facilitate legitimate trade between European companies and Iran. The other signatories to the original P5+1+EU agreement (the five permanent members of the United Nations Security Council – Britain, China, France, Russia, the US, plus Germany) – with Iran, China and Russia supported the EU move. China and the EU are Iran’s two biggest trading partners, and they accounted for more than half of Iran’s foreign trade last year. Their move could mean that Iran is unlikely to be paralyzed by the US sanction and forced back to the negotiation table any time soon.

Long-term implications for US dollar

The unprecedented EU action on Iranian trade in the face of US sanctions presents a long-term challenge to the pre-eminent position of the US dollar in the global financial system. The euro is a close second to the US dollar in global payment, as figure 1 shows, and if the Special Purpose Vehicle sponsored by the EU succeeds in preserving Iran’s foreign trade, some other countries could follow. If the list of countries the US imposes sanctions on keeps rising under President Trump’s administration, then there could be a tendency to move away from the US dollar as a medium of exchange in the global financial system and hurt the currency in the long run.

The pre-eminent position of the US dollar on international debt issuance, international loans, foreign exchange turnover and foreign exchange reserves often reflects the role of that of a vehicle currency. In the international debt in US dollars raised by company X in country A used for its project in country B, the USD's role is that of a vehicle currency to facilitate the investment and does not reflect any economic activities associated with the US. The situation is akin to the petrodollar's role after the oil crises. The extension of US sanctions to too many countries could discourage its use as a means of stored value by those countries.

There is no imminent challenger to the role of US dollar in the world today; no other currency can provide the US dollar liquidity on global financial transactions at the moment. The exorbitant privilege enjoyed by the US dollar has been there for more than half a century since the 1965 complaint, and it persists. However, the combined effect of exorbitant privilege and weaponization of the dollar could hurt the role of the US dollar in the long run. Whether the current dollar weaponization will or will not overstretch the said privilege remains to be seen.

Henry Chan is visiting senior research fellow at Cambodia Institute for Development and Peace. The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.