By Victor Zheng; Roger Luk |

chinawatch.cn |

Updated: 2019-03-07 15:27

Since the rollout of the Belt and Road Initiative (BRI) in 2013, views have been mixed around the world: optimistic, pessimistic or skeptical. Some take it as having economic, political and cultural challenges. Others see it as offering multidimensional development opportunities for mutual prosperity. There is no dearth of analyses from various perspectives, but objective evaluation of its outcomes and impacts is scarce.

The Global Competitiveness Report allows the comparative study of infrastructure development in BRI economies with the rest of the world, i.e. non-Belt and Road (non-BRI) economies.

For the Belt and Road economies, we adopt the classic definition of those along the Silk Road Economic Belt and the 21st-Century Maritime Silk Road. They cover Central Asia, West Asia, the Middle East, Continental Europe, South China Sea, the South Pacific, and the Indian Sub-Continent.

The index has been compiled by the internationally renowned World Economic Forum since 2005. It is based on 12 pillars -- institutions, infrastructure, the macroeconomic environment, health and primary education, higher education and training, goods market efficiency, labor market efficiency, financial market development, technological readiness, market size, business sophistication, and innovation.

In terms of GDP those selected 137 countries or economies accounted for over 98 percent of the world economy in 2018 and sufficiently representative.

As expected, the competitiveness scores of developed economies rank on top of the list and developing economies rank at the bottom. In terms of growth momentum, however, European and North American economies have been slackening in recent years, while developing economies in Asia, Africa and Latin America have been catching up.

Since the index covers most Belt and Road economies, the finding is reliable. Also, there are sufficient data for both cross-sectional and longitudinal comparisons.

The BRI advocates the five connectivities of policy coordination, facilities connectivity, unimpeded trade, financial integration and people-to-people bonds. Infrastructure, as the term implies, is essential and indispensable.

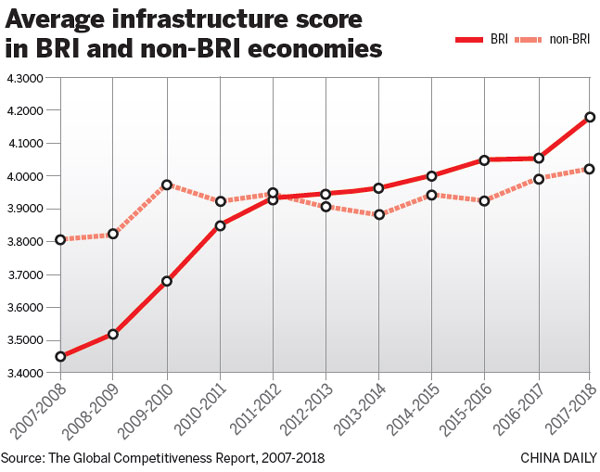

The "infrastructure" pillar in the index is used to illustrate comparative development between Belt and Road and non-Belt and Road economies. The Chinese mainland, Taiwan, Hong Kong and Macao are considered "host" economies and thus excluded.The average index score of infrastructure in BRI economies was far below that of the other economies in 2007. Five years later, their average scores were almost on par.

Following the commencement of the initiative, the average score of Belt and Road economies surpassed the non-Belt and Road region, and the gap is widening.

One may notice that the average score of infrastructure in Belt and Road economies has been rising since 2007, while that of the other economies has been stagnant since 2009. Stagnancy in these economies is explainable by the outbreak of the global "financial tsunami" in 2008 and its subsequent recession.

How could the Belt and Road economies still improve their infrastructure if they were not immune to the global economic downturn? The "BRI factor" might give a plausible explanation.

Infrastructure is the cornerstone of the economy and competitiveness is its determinant. With continuous improvement in infrastructure, Belt and Road economies also inject dynamism into their economies.

Thus, it may be roughly concluded that BRI has brought more significant changes to economies in BRI economies than non-BRI economies.

One might argue that despite skepticism and pessimism, it is evident that those on board BRI have benefited from infrastructural development. Apparently, more economies would wish to participate on realizing opportunities or potential to their benefit. A case in point is the change of mind of Japan in October last year.

Although the Global Competitiveness Index is compiled by a reputable body with reliable data through a professional approach and is undoubtedly objective and authoritative, there are still inadequacies to bear in mind.

First, not all countries or economies under the initiative are included.

Second, the index focuses on economic and financial factors, while other areas such as policy coordination and social relations are not covered. Thus, its impact could be understated.

Third, standards or criteria used in compiling the index can be improved by considering and addressing any inherent cultural biases.

Undoubtedly, the impact of ambitious, tremendous regional cooperation and integrated plans under the initiative will not be apparent in the short term. It will take time to develop and incubate.

The initial analysis shows that although the challenges are numerous, the potential and opportunities are equally large. A succinct description made by Deloitte Insight in 2018 is probably the best footnote of the first lustrum development.

“If we were to draw an analogy, it would be this: BRI is a journey, one with opportunities and risks, and one that — four [sic] years in — is still closer to its start than its end. That means investors need to take a longer view or projects than they are accustomed to doing. And while we do not downplay the risks, we believe they are less serve than many assume.”

Victor Zheng is co-convener of the Global China Research Programme of The Chinese University of Hong Kong. Roger Luk is a retired banker, an adjunct professor of business administration and honorary research fellow at the Hong Kong Institute of Asia-Pacific Studies.

The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.

Since the rollout of the Belt and Road Initiative (BRI) in 2013, views have been mixed around the world: optimistic, pessimistic or skeptical. Some take it as having economic, political and cultural challenges. Others see it as offering multidimensional development opportunities for mutual prosperity. There is no dearth of analyses from various perspectives, but objective evaluation of its outcomes and impacts is scarce.

The Global Competitiveness Report allows the comparative study of infrastructure development in BRI economies with the rest of the world, i.e. non-Belt and Road (non-BRI) economies.

For the Belt and Road economies, we adopt the classic definition of those along the Silk Road Economic Belt and the 21st-Century Maritime Silk Road. They cover Central Asia, West Asia, the Middle East, Continental Europe, South China Sea, the South Pacific, and the Indian Sub-Continent.

The index has been compiled by the internationally renowned World Economic Forum since 2005. It is based on 12 pillars -- institutions, infrastructure, the macroeconomic environment, health and primary education, higher education and training, goods market efficiency, labor market efficiency, financial market development, technological readiness, market size, business sophistication, and innovation.

In terms of GDP those selected 137 countries or economies accounted for over 98 percent of the world economy in 2018 and sufficiently representative.

As expected, the competitiveness scores of developed economies rank on top of the list and developing economies rank at the bottom. In terms of growth momentum, however, European and North American economies have been slackening in recent years, while developing economies in Asia, Africa and Latin America have been catching up.

Since the index covers most Belt and Road economies, the finding is reliable. Also, there are sufficient data for both cross-sectional and longitudinal comparisons.

The BRI advocates the five connectivities of policy coordination, facilities connectivity, unimpeded trade, financial integration and people-to-people bonds. Infrastructure, as the term implies, is essential and indispensable.

The "infrastructure" pillar in the index is used to illustrate comparative development between Belt and Road and non-Belt and Road economies. The Chinese mainland, Taiwan, Hong Kong and Macao are considered "host" economies and thus excluded.The average index score of infrastructure in BRI economies was far below that of the other economies in 2007. Five years later, their average scores were almost on par.

Following the commencement of the initiative, the average score of Belt and Road economies surpassed the non-Belt and Road region, and the gap is widening.

One may notice that the average score of infrastructure in Belt and Road economies has been rising since 2007, while that of the other economies has been stagnant since 2009. Stagnancy in these economies is explainable by the outbreak of the global "financial tsunami" in 2008 and its subsequent recession.

How could the Belt and Road economies still improve their infrastructure if they were not immune to the global economic downturn? The "BRI factor" might give a plausible explanation.

Infrastructure is the cornerstone of the economy and competitiveness is its determinant. With continuous improvement in infrastructure, Belt and Road economies also inject dynamism into their economies.

Thus, it may be roughly concluded that BRI has brought more significant changes to economies in BRI economies than non-BRI economies.

One might argue that despite skepticism and pessimism, it is evident that those on board BRI have benefited from infrastructural development. Apparently, more economies would wish to participate on realizing opportunities or potential to their benefit. A case in point is the change of mind of Japan in October last year.

Although the Global Competitiveness Index is compiled by a reputable body with reliable data through a professional approach and is undoubtedly objective and authoritative, there are still inadequacies to bear in mind.

First, not all countries or economies under the initiative are included.

Second, the index focuses on economic and financial factors, while other areas such as policy coordination and social relations are not covered. Thus, its impact could be understated.

Third, standards or criteria used in compiling the index can be improved by considering and addressing any inherent cultural biases.

Undoubtedly, the impact of ambitious, tremendous regional cooperation and integrated plans under the initiative will not be apparent in the short term. It will take time to develop and incubate.

The initial analysis shows that although the challenges are numerous, the potential and opportunities are equally large. A succinct description made by Deloitte Insight in 2018 is probably the best footnote of the first lustrum development.

“If we were to draw an analogy, it would be this: BRI is a journey, one with opportunities and risks, and one that — four [sic] years in — is still closer to its start than its end. That means investors need to take a longer view or projects than they are accustomed to doing. And while we do not downplay the risks, we believe they are less serve than many assume.”

Victor Zheng is co-convener of the Global China Research Programme of The Chinese University of Hong Kong. Roger Luk is a retired banker, an adjunct professor of business administration and honorary research fellow at the Hong Kong Institute of Asia-Pacific Studies.

The author contributed this article to China Watch exclusively. The views expressed do not necessarily reflect those of China Watch.

All rights reserved. Copying or sharing of any content for other than personal use is prohibited without prior written permission.